healthmyths

Platinum Member

- Sep 19, 2011

- 29,508

- 10,919

- 900

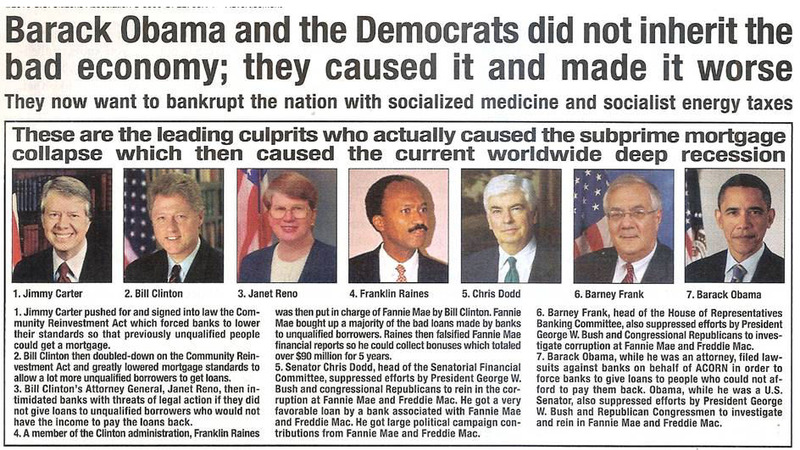

I looked through this entire article and NOT one mention that George W Bush single-handedly caused the crisis as many Bush bashers believe!

And while GWB was NOT single-handedly blamed as MOST unintelligent UNINFORMED idiots would have you believe..

Here are the Presidents that share the blame.

[Personal note: Unlike many of the posters here I am intellectually honest to include GOP as part of the blame... Yes GWB included!]

These people were appointed by US Presidents including Reagan, Bush Senior, Clinton, Bush and Obama to top government positions, in part as a payback for campaign contribution by some of these Wall Street firms.

Who contributed to the creation to the financial crisis and the ensuing economic crisis?

The following is a general answer followed by a section naming the key players:

Regulators who relaxed risk management regulations required by the banks and for not regulating derivative investments (please, see more specific details below)

The Federal Reserve Chairmen who dismissed the build-up of the housing bubble from 2002 to 2007 until it was too late. They did not take actions to regulate mortgage companies or control the housing bubble

World Central Bankers who blindly copied the US Federal Reserve Bank policies

World Financial Regulators who blindly copied US financial market models and regulations

World Investment Banks who sold subprime (high risk) mortgage backed securities to their customers without fully understanding them and who hired credit rating agencies to rate them as high quality investment when in fact they included high risk loans. The same banks who sold the subprime investments later bet against their own clients without disclosing the conflict of interest to their clients

Credit Rating Agencies who overrated junk securities as investment-grade quality and misled investors about the risk and the value of these investments

Academic and Financial Economists who ignored the warnings and misjudged macroeconomic and financial market indicators

Award-winning Economists who designed flawed risk pricing models

Investment Analysts who used flawed risk pricing models and asset portfolio theories

Wall Street Banking Executives who ignored internal risk management policies out of greed to increase revenues and their bonuses in the short term at the expense of long term stability of their companies

Wall Street Boards of Directors who did not protect their shareholders against excessive executive compensation and ignored prudent risk management strategies

Wall Street Advisors who did not do their homework before advising their clients on bad investments

Investment Fund Managers who lost billions of dollars investing without adequate due diligence

Mortgage Brokers who sold loans to unqualified borrowers in order to collect more commissions

Homebuyers who took loans they could not afford to pay back and blamed the banks for predatory lending

US Presidents for hiring former Wall Street lobbyists as government policy makers who bailed out the banks without regard to the moral hazard. By doing so, they shifted the burden on the taxpayers and risked the future of the national economy

US Supreme Court Justices who ruled that the government may not ban political spending by corporations in candidate elections thus tightening the grip of Wall Street on government officials and skewing the balance of power in favor of Wall Street and big companies.

The Financial Media who took no responsibility for promoting the illusions of a healthy housing sector and for not asking the right questions. Media outlets that favored a promotional business model at the expense of investigative journalism. In our research, we found a prevalent bias in allocating airwaves and print space to brand name experts. Most journalists and editors seem to ignore voices that are not well-known or those who have a story that do not fit their narrative or preconception. All we had to do is Google simple phrases like "US Economic Risks" to find a wealth of information that would raise so many critical questions. If equal media exposure was given to the voices that warned us about the housing bubble, the damage could have been mitigated.

Who is to Blame for the Financial Crisis and Ensuing Economic Crisis

And while GWB was NOT single-handedly blamed as MOST unintelligent UNINFORMED idiots would have you believe..

Here are the Presidents that share the blame.

[Personal note: Unlike many of the posters here I am intellectually honest to include GOP as part of the blame... Yes GWB included!]

These people were appointed by US Presidents including Reagan, Bush Senior, Clinton, Bush and Obama to top government positions, in part as a payback for campaign contribution by some of these Wall Street firms.

Who contributed to the creation to the financial crisis and the ensuing economic crisis?

The following is a general answer followed by a section naming the key players:

Regulators who relaxed risk management regulations required by the banks and for not regulating derivative investments (please, see more specific details below)

The Federal Reserve Chairmen who dismissed the build-up of the housing bubble from 2002 to 2007 until it was too late. They did not take actions to regulate mortgage companies or control the housing bubble

World Central Bankers who blindly copied the US Federal Reserve Bank policies

World Financial Regulators who blindly copied US financial market models and regulations

World Investment Banks who sold subprime (high risk) mortgage backed securities to their customers without fully understanding them and who hired credit rating agencies to rate them as high quality investment when in fact they included high risk loans. The same banks who sold the subprime investments later bet against their own clients without disclosing the conflict of interest to their clients

Credit Rating Agencies who overrated junk securities as investment-grade quality and misled investors about the risk and the value of these investments

Academic and Financial Economists who ignored the warnings and misjudged macroeconomic and financial market indicators

Award-winning Economists who designed flawed risk pricing models

Investment Analysts who used flawed risk pricing models and asset portfolio theories

Wall Street Banking Executives who ignored internal risk management policies out of greed to increase revenues and their bonuses in the short term at the expense of long term stability of their companies

Wall Street Boards of Directors who did not protect their shareholders against excessive executive compensation and ignored prudent risk management strategies

Wall Street Advisors who did not do their homework before advising their clients on bad investments

Investment Fund Managers who lost billions of dollars investing without adequate due diligence

Mortgage Brokers who sold loans to unqualified borrowers in order to collect more commissions

Homebuyers who took loans they could not afford to pay back and blamed the banks for predatory lending

US Presidents for hiring former Wall Street lobbyists as government policy makers who bailed out the banks without regard to the moral hazard. By doing so, they shifted the burden on the taxpayers and risked the future of the national economy

US Supreme Court Justices who ruled that the government may not ban political spending by corporations in candidate elections thus tightening the grip of Wall Street on government officials and skewing the balance of power in favor of Wall Street and big companies.

The Financial Media who took no responsibility for promoting the illusions of a healthy housing sector and for not asking the right questions. Media outlets that favored a promotional business model at the expense of investigative journalism. In our research, we found a prevalent bias in allocating airwaves and print space to brand name experts. Most journalists and editors seem to ignore voices that are not well-known or those who have a story that do not fit their narrative or preconception. All we had to do is Google simple phrases like "US Economic Risks" to find a wealth of information that would raise so many critical questions. If equal media exposure was given to the voices that warned us about the housing bubble, the damage could have been mitigated.

Who is to Blame for the Financial Crisis and Ensuing Economic Crisis