Cougarbear

Gold Member

- Jan 29, 2022

- 9,153

- 4,028

- 208

I didn't know where to put this but has anyone ever looked closely to whole life insurance and universal life insurance and the scam cash value and dividends are? Whole life has an insurance component of decreasing term. Decreasing term means the premium stays the same but the cost of the insurance portion of the premium is going up so the coverage has to go down if the client pays the same premium. The premium is made up of the mortality cost and company expenses including commissions. The client is overcharged for the cost of insurance and expenses and the overcharge is put into a savings vehicle called "cash value." When the covered person dies, the company pays out the death benefit but keeps the cash value. Or, they pay the decreasing turn portion and the cash value. The interest rates, premiums and cash value are all guaranteed.

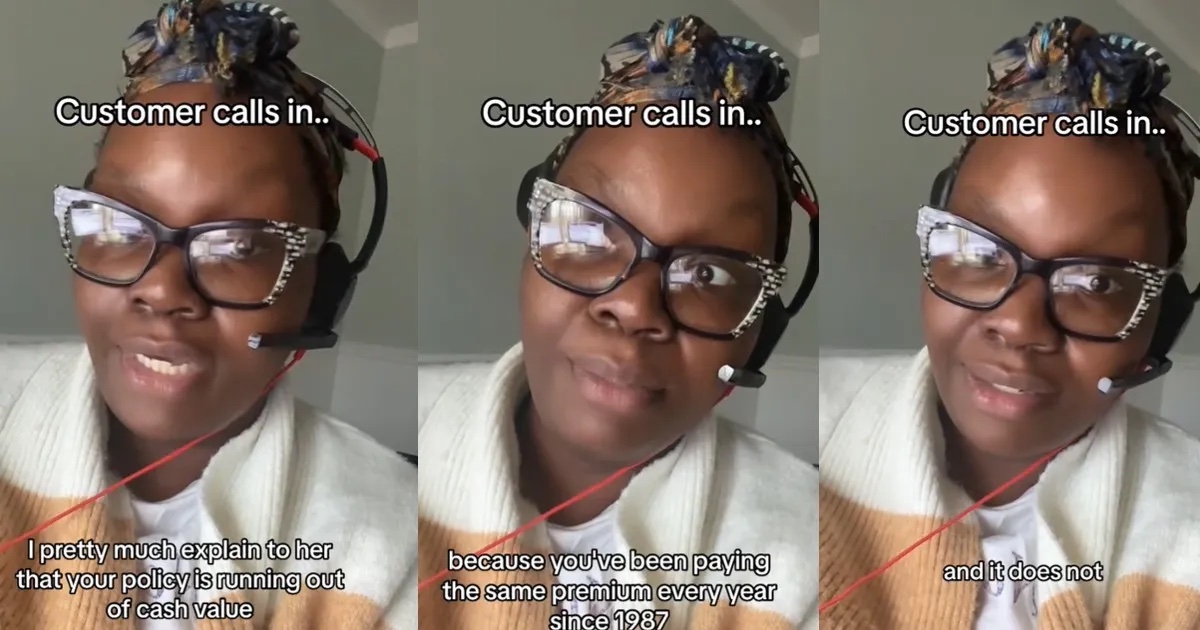

Universal life has annual renewable term as the insurance. The mortality cost rises each year but the coverage stays the same. Clients again are overcharged and the overcharged goes into the general account of the insurance company called cash value. It can grow like whole life. However, the interest, premiums and cash value are not guaranteed. Even if the cash is put into a separate indexed or investment fund account. After 15-20 years, the mortality cost reaches what the client is paying for their premium. After that, the mortality cost continues to rise above the premiums. The company doesn't ask for more premium. Instead, they begin to take money out of the cash value to pay for the rising mortality cost, the actual cost for the insurance. When people reach retirement and expect to have some supplemental retirement income, they find out that the insurance company has stolen all their cash. Here is a customer service representative of a large life insurance company explaining this legalized fraud. You can find the actual video on Tiktok...But here is the transcript of the video.

Universal life has annual renewable term as the insurance. The mortality cost rises each year but the coverage stays the same. Clients again are overcharged and the overcharged goes into the general account of the insurance company called cash value. It can grow like whole life. However, the interest, premiums and cash value are not guaranteed. Even if the cash is put into a separate indexed or investment fund account. After 15-20 years, the mortality cost reaches what the client is paying for their premium. After that, the mortality cost continues to rise above the premiums. The company doesn't ask for more premium. Instead, they begin to take money out of the cash value to pay for the rising mortality cost, the actual cost for the insurance. When people reach retirement and expect to have some supplemental retirement income, they find out that the insurance company has stolen all their cash. Here is a customer service representative of a large life insurance company explaining this legalized fraud. You can find the actual video on Tiktok...But here is the transcript of the video.

72-Year-Old Is Told By Life Insurance Company That Her Policy Is Worthless Because She’s Paid For 40 Years

This is indefensible.

twistedsifter.com