Andylusion

Platinum Member

You mean CNBC is a harbinger of liberals? lol

How about Faux or WSJ, ANYTHING

How about the WORLD WIDE CREDIT BUBBLE, CRA TOO? How about the bubble in the commercial markets and auto industry in the 2000's too? CRA? LOL

Yes, indeed.

[ame="https://www.youtube.com/watch?v=aW2V50AS7K0"]Look how disdainfully they treat Dr Ron Paul .[/ame]

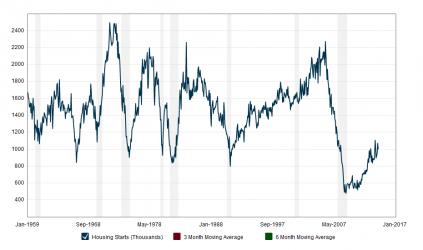

.

.

Weird, so politicians taking 2 minutes a piece on opening statements (about 15 per committee) and criticizing them means Paul's nonsense has credibility? lol

ONE MORE TIME, HOW THE FUCK DOES CRA CREATE A WORLD WIDE CREDIT BUBBLE? Or one in the auto industry or commercial real estate? Grow a fkkng brain and get honest!!!

It doesn't. How is that relevant?

Just because two different countries, have an economic crash, mean it's impossible for the specific policies that caused our crash, can't be CRA. There is no reason to assume that every economic crash in the universe, must have a common cause, because they had a common time frame.

When you have unstable fiscal policy in multiple countries that have interdependent economies, when one economy takes a dive, it affects the others. If other countries have bad policies too, it can cause them to crash.

Canada did not have CRA, or Glass Steagall, and did not crash.

It's a leap of logic to assume that because another country did have a crash, and didn't have CRA, means it can't possibly be the cause of our crash.

Right Wing Versions of Political Events Challenged

Right Wing Versions of Political Events Challenged I know: Representative Frank is a co-sponsor of a GOP sponsored resolution in the year 2005. Why is 2005 so important?

I know: Representative Frank is a co-sponsor of a GOP sponsored resolution in the year 2005. Why is 2005 so important?