Dad2three

Gold Member

Just how many LIES do we have to catch this asshole, Dud2three before we simply ignore him, he's on par with KNoB, and Franco!....OCD is his friend!

Care to point out ONE lie from me dickhead? Didn't think you could!

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

Unlock unbeatable offers today. Shop here: https://amzn.to/4cEkqYs 🎁

Just how many LIES do we have to catch this asshole, Dud2three before we simply ignore him, he's on par with KNoB, and Franco!....OCD is his friend!

READ THE POST YOU STUPID ASS

I said, "he could walk on water" and it would not matter right now.

The poll shows a significant portion of the population thinks he sucks.

That does not make them right or wrong. It is their opinion.

Opinions, are like assholes...I like FACTUAL data. Dubya lost 673,000+ PRIVATE sector jobs in 8 years and 5+ million have been created under Obama. That's just one data point!

If the econony under President Obama helped to create that many jobs, why did Harry Reid push for federal unemployment extensions as a priority earlier this year, while the House didn't feel we could afford it under this administration's skyrocketing national debt and losing our AAA credit rating for the first time in our nation's history?

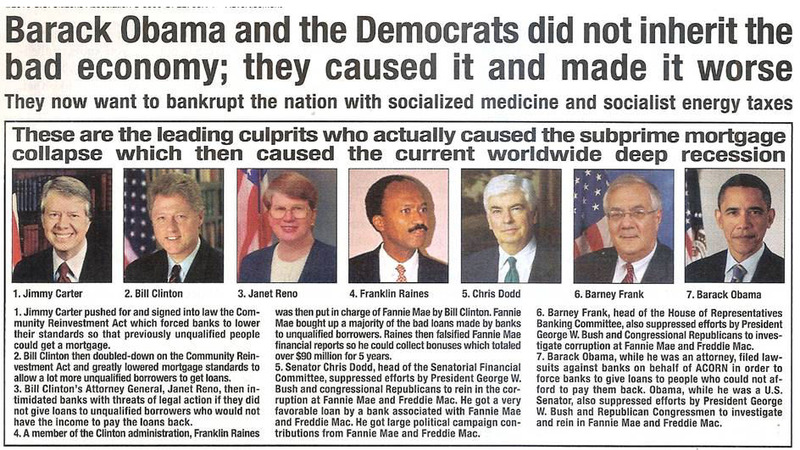

FACT: Liberal Public Policy caused the mortgage crisis by mandating eased requirements for lending, even to people who had no chance of ever paying the loan back. If banks and other lending institutions did not comply, their "score" from the SEC was too low to permit certain business transactions such as merges, etc. This is nothing less than a gun held to the head.

FACT: Many lending institutions were sued or otherwise pressured by ACORN, forcing them to make loans to folks who didn't qualify nor had any chance of ever repaying that loan.

FACT: HUD (Housing and Urban Development) under Andrew Cuomo, head of HUD) browbeat banks to make loans to folks who they knew couldn't pay them back.

FACT: Many lending institutions were sued or otherwise pressured by ACORN, forcing them to make loans to folks who didn't qualify nor had any chance of ever repaying that loan. IN FACT, BARACK OBAMA WAS INVOLVED IN AT LEAST ONE OF THESE LAWSUITS

FACT: Fannie Mae's sole purpose for being was to offer a Federal Guarantee of loans. So banks and other lending institutions didn't need to worry about thing. If a loan went bad, Fannie Mae was there to pick up the pieces (until there were too many pieces to pick up)

FACT: The Democrats stacked the operations of Fannie Mae with other Democrats who then cooked the books (FM had to pay MILLIONS in fines to the SEC over this) and took HUNDREDS OF MILLIONS OF DOLLARS in bonuses and funneled MILLIONS in campaign contributions to members of Congress. Franklin Raines (part of the Obama Administration) personally took 90 million dollars despite Fannie Mae's fines and fraud.

FACT: Bill Clinton turned a blind eye to all of this during most of the 90's. In fact, he worsened the situation in 1995 by making the CRA even more lopsided and requiring even MORE bad loans. One thing he did was to force lending institutions to accept up to 31% of one's income for a mortgage whereas previously it was only 25%

FACT: The Democrats who run Fannie Mae took hundreds of millions in bonuses while Congressional Dems provided cover, including Charlie Rangel , Chris Dodd , Barack Obama and Joe Biden.

FACT: Democrat Chris Dodd was #1 recipient with Democrat Barack Obama being #2 in campaign contributions from Fannie Mae and Freddy Mac

FACT: The Democrats blocked every attempt by Republicans to investigate Fannie Mae and its business practices. In fact, the Bush Administration made over 30 attempts over his two terms in office only to have the Democrats block every one through parliamentary procedures as the Republicans, while controlling both Houses, NEVER had a super majority so the Dems could block anything they pleased (case in point - judicial nominees)

http://query.nytimes.com/gst/fullpag...gewanted=print

Quote:

September 11, 2003

New Agency Proposed to Oversee Freddie Mac and Fannie Mae

By STEPHEN LABATON

WASHINGTON, Sept. 10 The Bush administration today recommended the most significant regulatory overhaul in the housing finance industry since the savings and loan crisis a decade ago.

Under the plan, disclosed at a Congressional hearing today, a new agency would be created within the Treasury Department to assume supervision of Fannie Mae and Freddie Mac, the government-sponsored companies that are the two largest players in the mortgage lending industry.

Note the date

Quote:

New Agency Proposed to Oversee Freddie Mac and Fannie Mae

By STEPHEN LABATON

WASHINGTON, Sept. 10 The Bush administration today recommended the most significant regulatory overhaul in the housing finance industry since the savings and loan crisis a decade ago.

Under the plan, disclosed at a Congressional hearing today, a new agency would be created within the Treasury Department to assume supervision of Fannie Mae and Freddie Mac, the government-sponsored companies that are the two largest players in the mortgage lending industry.

The new agency would have the authority, which now rests with Congress, to set one of the two capital-reserve requirements for the companies. It would exercise authority over any new lines of business. And it would determine whether the two are adequately managing the risks of their ballooning portfolios.

The plan is an acknowledgment by the administration that oversight of Fannie Mae and Freddie Mac -- which together have issued more than $1.5 trillion in outstanding debt -- is broken. A report by outside investigators in July concluded that Freddie Mac manipulated its accounting to mislead investors, and critics have said Fannie Mae does not adequately hedge against rising interest rates.

http://www.bucksright.com/bush-propo...n-in-2003-1141

Quote:

A September 11, 2003 New York Times article shows that President Bush proposed the most significant regulatory overhaul in the housing finance industry since the savings and loan crisis a decade ago. His proposal: An agency within the Treasury Department to supervise mortgage giants Fannie Mae and Freddie Mac.

Fearing that mortgages would no longer be available to people who were unable to pay them back, Democrats eventually killed the proposal. The current meltdown in the mortgage industry is a direct result of giving mortgages to people who could not pay them back, a practice protected by Congressional Democrats.

Both entities were recently taken over by the government, a move that puts trillions of taxpayer dollars at risk.

Under the plan, disclosed at a Congressional hearing today, a new agency would be created within the Treasury Department to assume supervision of Fannie Mae and Freddie Mac, the government-sponsored companies that are the two largest players in the mortgage lending industry.

The new agency would have the authority, which now rests with Congress, to set one of the two capital-reserve requirements for the companies. It would exercise authority over any new lines of business. And it would determine whether the two are adequately managing the risks of their ballooning portfolios.

The plan is an acknowledgment by the administration that oversight of Fannie Mae and Freddie Mac which together have issued more than $1.5 trillion in outstanding debt is broken. A report by outside investigators in July concluded that Freddie Mac manipulated its accounting to mislead investors, and critics have said Fannie Mae does not adequately hedge against rising interest rates.

But Democrats in Congress, also known as the caucus perpetually on the wrong side of history, were having none of this responsibility stuff.

These two entities Fannie Mae and Freddie Mac are not facing any kind of financial crisis, said Representative Barney Frank of Massachusetts, the ranking Democrat on the Financial Services Committee. The more people exaggerate these problems, the more pressure there is on these companies, the less we will see in terms of affordable housing.

Representative Melvin L. Watt, Democrat of North Carolina, agreed.

I dont see much other than a shell game going on here, moving something from one agency to another and in the process weakening the bargaining power of poorer families and their ability to get affordable housing, Mr. Watt said.

The proposal worked its way around Congress for a couple of years. Efforts at reform of the kind proposed by President Bush were shot down by Democrats each time.

In 2005, Republican Mike Oxley, then chairman of the House Financial Services Committee, brought up a reform bill (H.R. 1461), and Fannie and Freddies lobbyists set out to weaken it.

[...]

During this period, Sen. Richard Shelby led a small group of legislators favoring reform, including fellow Republican Sens. John Sununu, Chuck Hagel and Elizabeth Dole. Meanwhile, [Democrat in bed with the mortgage industry Chris] Dodd who along with Democratic Sens. John Kerry, Barack Obama and Hillary Clinton were the top four recipients of Fannie and Freddie campaign contributions from 1988 to 2008 actively opposed such measures and further weakened existing regulation.

According to OpenSecrets.org, between 1988 and 2008 Dodd received $133,900, Kerry $111,000, Clinton $75,550, and Obama in only 143 days in the Senate received a whopping $105,849 from Fannie Mae and Freddie Mac.

Pennsylvania Democrat representative Paul Kanjorksi, who also opposed new Fannie Mae and Freddie Mac regulations, was given more than any other member of the House of Representatives. He was paid $65,500 by representatives of these entities.

And, in case you were wondering, John McCain co-sponsored a bill requiring greater Fannie Mae / Freddie Mac regulation in 2005. It was also blocked procedurally by Democrats.

The 2003 New York Times article was unearthed by a Free Republic poster.

UPDATE: 2004 video posted to YouTube shows Republicans arguing for, and Democrats arguing against, regulations that would have saved us from the current crisis.

http://www.bucksright.com/congressma...ge-crisis-1451

Quote:

Congressman Sorry Democrats Dropped Ball On Mortgage Crisis

Wed, Oct 1, 2008 at 10:55 am Posted by Steven in Economy

After being featured on Hannity & Colmes in a damning 2004 video showing Democrats fighting tooth-and-nail against greater Fannie Mae and Freddie Mac regulations, Democrat Congressman Artur Davis admits Democrats dropped the ball on reigning in the failed institutions and calls on fellow Democrats to do the same.

Like a lot of my Democratic colleagues, I was too slow to appreciate the recklessness of Fannie Mae and Freddie Mac. I defended their efforts to encourage affordable homeownership, when in retrospect I should have heeded the concerns raised by their regulator in 2004. Frankly, I wish my Democratic colleagues would admit that when it comes to Fannie and Freddie, we were wrong. By the way, I wish my Republican colleagues would admit that they missed the early warning signs that Wall Street deregulation was overheating the securities market and promoting dangerously lax lending practices. When it comes to the debacle in our capital markets, there is much blame to go around for both sides.

Along with President Clinton, I take issue with Davis contention that equal blame exists on both sides. President Bush requested greater oversight in 2003, Republicans are clearly seen in the video fighting for greater oversight in 2004, and John McCain led the charge for greater oversight in 2005. All efforts were rebuffed by Democrats, who demagogued the issue with racial politics that made reform impossible to accomplish. At least they tried. I see no evidence of any push toward greater Fannie Mae / Freddie Mac oversight since the short bus rolled onto Capitol Hill in January 2007.

That said, I appreciate Congressman Davis candor in admitting Democrats let their ideology get in the way of what was right for the country.

MORE RIGHT WING GARBAGE, I'm shocked

Q When did the Bush Mortgage Bubble start?

A The general timeframe is it started late 2004.

Let's take a look at that timeline under President Bush directly from the mouths of our representatives in Congress, and the mortgage crisis through the government oversight of Freedie Mae and Freddie Mac.

September 1999

With pressure from the Clinton Administration, Fannie Mae eased credit requirements on loans it would purchase from lenders, making it easier for banks to lend to borrowers unqualified for conventional loans. Raines explained that "there remain too many borrowers whose credit is just a notch below what our underwriting has required who have been relegated to paying significantly higher mortgage rates in the so-called subprime market," reported the New York Times.

With this action, Fannie Mae put itself at substantial risk in the event of an economic downturn. "From the perspective of many people, including me, this is another thrift industry growing up around us," warned Peter Wallison. "If they fail, the government will have to step up and bail them out the way it stepped up and bailed out the thrift industry." The danger was known.

March 2000

Rep. Richard Baker (R-Louisiana) proposed a bill to reform Fannie and Freddie's oversight in a House Subcommittee on Capital Markets.

Rep. Frank (D-Massachusetts) dismissed the idea, saying concerns about the two were "overblown" and that there was "no federal liability there whatsoever."

June 2000

Rep. Marge Roukema (R-New Jersey): "very few banks or S&Ls could, even in this day and age, even now, meet the stress-testing requirements which Fannie and Freddie are required to meet."

Rep. Carolyn Maloney (D-New York) regarding the Treasury Department line of credit: "It is really symbolic, it is obsolete, it has never been used." "Would you explain why it would be important to repeal something that seems to be of little use?"

Smith: "as long as the pipeline is there, it is like it is very expandable. . . . It is only $2 billion today. It could be $200 billion tomorrow."

Because of Democrat obfuscation, Smith's "tomorrow" arrived in 2008 when Treasury Secretary Henry Paulson put Fannie and Freddie into conservatorship.

February 2003

OFHEO reports that "although investors perceive an implicit Federal guarantee of [GSE] obligations . . . the government has provided no explicit legal backing for them," warning that unexpected problems at a GSE could immediately spread into financial sectors beyond the housing market, according to a White House release.

June 2003

Freddie Mac reported it had understated its profits by $6.9 billion. OFHEO director Armando Falcon Jr. requested that the White House audit Fannie Mae.

July 2003

Sens. Chuck Hagel (R-Nebraska), Elizabeth Dole (R-North Carolina) and John Sununu (R-New Hampshire) introduced legislation to address Regulation of Fannie Mae and Freddie Mac. The bill was blocked by Democrats.

September 2003

In an interview with Ron Insana for CNN Money, Rep. Baker warned, "I have concerns that if appropriate resources aren't allocated for internal risk management, the consequences will be far more severe than just a real estate slowdown. The losses would fall quickly through the capital these companies have and down to shareholders and taxpayers. These companies have some of the lowest capital margins of any financial institution in the nation, yet, at the same time, they are two of the largest. The concern is that if something doesn't work out the way they predict, the American taxpayer could be called on to pay off the debt in some sort of bailout."

Rep. Barney Frank (D-Massachusetts): "These two entities - Fannie Mae and Freddie Mac - are not facing any kind of financial crisis. . . . The more people exaggerate these problems, the more pressure there is on these companies, the less we will see in terms of affordable housing."

October 2003

Fannie Mae discloses $1.2 billion accounting error.

November 2003

Council of the Economic Advisers Chairman Greg Mankiw warned, "The enormous size of the mortgage-backed securities market means that any problems at the GSEs matter for the financial system as a whole. This risk is a systemic issue also because the debt obligations of the housing GSEs are widely held by other financial institutions. The importance of GSE debt in the portfolios of other financial entities means that even a small mistake in GSE risk management could have ripple effects throughout the financial system," from a White House release.

February 2004

Mankiw cautions Congress to "not take [the financial market's] strength for granted." Again, the call from the Administration was to reduce this risk by "ensuring that the housing GSEs are overseen by an effective regulator," says a White House release.

OFHEO reported that Fannie Mae and CEO Raines had manipulated its accounting to overstate its profits. Congress and the Bush administration sought strong new regulation and authority to put the GSEs under conservatorship if necessary. As the Washington Post reports, Fannie Mae and Freddie Mac responded by orchestrating a major campaign "by traditional allies including real estate agents, home builders and mortgage lenders. Fannie Mae ran radio and television ads ahead of a key Senate committee meeting, depicting a Latino couple who fretted that if the bill passed, mortgage rates would go up." Again, GSE pressure prevailed.

October 2004

In a subcommittee testimony, Democrats vehemently reject regulation of Fannie Mae in the face of dire warning of a Fannie Mae oversight report. A few of them, Black Caucus members in particular, are very angry at the OFHEO Director as they attempt to defend Fannie Mae and protect their CRA extortion racket.

Rep. Maxine Waters (D-California): "Through nearly a dozen hearings where, frankly, we were trying to fix something that wasn't broke."

Rep. Maxine Waters (D-California): "Mr. Chairman, we do not have a crisis at Freddie Mac, and particularly at Fannie Mae, under the outstanding leadership of Mr. Frank Raines."

Rep. Ed Royce (R-California): "In addition to our important oversight role in this committee, I hope that we will move swiftly to create a new regulatory structure for Fannie Mae, for Freddie Mac, and the federal home loan banks."

Rep. Lacy Clay (D-Missouri): "This hearing is about the political lynching of Franklin Raines."

Rep. Ed Royce (R-California): "There is a very simple solution. Congress must create a new regulator with powers at least equal to those of other financial regulators, such as the OCC or Federal Reserve."

Rep. Barney Frank (D-Massachusetts): "Uh, I, this, you, you, you seem to me saying, Well, these are in areas which could raise safety and soundness problems.' I don't see anything in your report that raises safety and soundness problems."

Rep. Maxine Waters (D-California): "Under the outstanding leadership of Mr. Frank Raines, everything in the 1992 Act has worked just fine. In fact, the GSEs have exceeded their housing goals. What we need to do today is to focus on the regulator, and this must be done in a manner so as not to impede their affordable housing mission, a mission that has seen innovation flourish from desktop underwriting to 100% loans."

Rep. Don Manzullo (R-Illinois): "Mr. Raines, 1.1 million bonus and a $526,000 salary. Jamie Gorelick, $779,000 bonus on a salary of 567,000. This is, what you state on page eleven is nothing less than staggering."

Rep. Don Manzullo (R-Illinois): "The 1998 earnings per share number turned out to be $3.23 and 9 mills, a result that Fannie Mae met the EPS maximum payout goal right down to the penny."

Rep. Don Manzullo (R-Illinois): "Fannie Mae understood the rules and simply chose not to follow them that if Fannie Mae had followed the practices, there wouldn't have been a bonus that year."

"The bill prohibited the GSEs from holding portfolios, and gave their regulator prudential authority (such as setting capital requirements) roughly equivalent to a bank regulator. In light of the current financial crisis, this bill was probably the most important piece of financial regulation before Congress in 2005 and 2006," reports the Wall Street Journal.

Greenspan testified that the size of GSE portfolios "poses a risk to the global financial system. It would be difficult, if not impossible, to bail out the lenders [GSEs] . . . should one get into financial trouble." He added, "If we fail to strengthen GSE regulation, we increase the possibility of insolvency and crisis . . . We put at risk our ability to preserve safe and sound financial markets in the United States, a key ingredient of support for homeownership."

Greenspan warned that if the GSEs "continue to grow, continue to have the low capital that they have, continue to engage in the dynamic hedging of their portfolios, which they need to do for interest rate risk aversion, they potentially create ever-growing potential systemic risk down the road . . . We are placing the total financial system of the future at a substantial risk."

Bloomberg writes, "If that bill had become law, then the world today would be different. . . . But the bill didn't become law, for a simple reason: Democrats opposed it on a party-line vote in the committee, signaling that this would be a partisan issue. Republicans, tied in knots by the tight Democratic opposition, couldn't even get the Senate to vote on the matter. That such a reckless political stand could have been taken by the Democrats was obscene even then."

April 2007

In "A Nightmare Grows Darker," the New York Times writes that the "democratization of credit" is "turning the American dream of homeownership into a nightmare for many borrowers." The "newfangled mortgage loans" called "affordability loans" "represent 60 percent of foreclosures."

2007-2008

The housing bubble began to burst, bad mortgages began to default, and finally the Fannie Mae and Freddie Mac portfolios were revealed to be what they were, in collapse. And the testimony is evident as to why. As Wallison noted, "Fannie and Freddie were, I would say, the poster children for corporate welfare."

Archived-Articles: Why the Mortgage Crisis Happened

Can't argue with a poll....if it really exists.

Peoples perceptions are what they are.

Which is consistent....after all, Reagan barely won re-election in 1984 with only 49....oh, wait.

And Obama won 50%+ in two straight elections, something Ronnie DIDN'T do. Go figure

Very wrong. Ronald Reagan won more than 50% of the popular vote in both 1980 and 1984.

And in 1980 it was with John Anderson, a Republican running a 3rd party campaign that pretty much took most of its support (just over 5% IIRC) from would be Reagan voters.

The worst part is that my tax dollars pay Dad2 to spread his Progressive disinformation

Just how many LIES do we have to catch this asshole, Dud2three before we simply ignore him, he's on par with KNoB, and Franco!....OCD is his friend!

Just how many LIES do we have to catch this asshole, Dud2three before we simply ignore him, he's on par with KNoB, and Franco!....OCD is his friend!

Just how many LIES do we have to catch this asshole, Dud2three before we simply ignore him, he's on par with KNoB, and Franco!....OCD is his friend!

If the public opinion and views of Democrats citing that NOTHING is wrong with Fannie and Freddie "under the outstanding leadership of Raines" is not enough to convince him, and stating his articles carry more weight, then he is in flat out denial and won't hear the truth.

BUT OBAMA IS STILL THE WORST PRESIDENT!!!

Gallup.Com - Polling Matters by Frank Newport: The Science of Ranking U.S. Presidents

The worst part is that my tax dollars pay Dad2 to spread his Progressive disinformation

Q When did the Bush Mortgage Bubble start?

A The general timeframe is it started late 2004.

funny watching the rightwingnut loons claim everyone else is lying.