McRocket

Gold Member

- Apr 4, 2018

- 5,031

- 707

- 275

- Banned

- #1

'Tomorrow, the US Department of Commerce will report its advance estimate of 2Q GDP which will be the long-awaited evidence that “Trumponomics” is working. The current estimates for the initial print run the gamut from 3.9% to over 5% annualized growth. Regardless of the actual number, the White House spokesman will be quick to take credit for success in turning America’s economy around.

...

Secondly, while the print will undoubtedly be a strong one, and not unexpected following a weak Q1 growth rate, the question is whether it is sustainable? A recent note from Goldman Sachs suggests some caution:

“An unusually large number of one-off factors appear to have boosted 2Q GDP, many of which are directly related to escalating trade concerns. As companies and countries race to secure supplies that may become expensive later on, exports have surged and inventories have swelled. If these trends are one-time adjustments (and our economists believe they are), the ‘payback’ in 2H could be significant. Enjoy the 2Q GDP number, which may be the last best print for a while.”

This is likely correct. As 2018 has seen a steady increase in trade tensions, and trade actions, between the US and its trading partners, we have already begun to see some of the negative impacts from those actions. Just this past week Boeing ($BA), General Motors ($GM) and Whirlpool ($WHR) all had disappointing reports with comments directly related to the negative impact of tariffs on their results. They are surely not going to be the last as the US has slapped tariffs on washing machines and solar panels in January, on steel and aluminum in March, and on US$34 billion of goods from China on July 6. Now, the administration is talking about another 25% tariff on close to $200 billion in foreign-made automobiles later this year.

Morgan Stanley also made very similar comments in their recent analysis about the unusually large number of one-off factors which appear to have boosted 2Q GDP, most of which are directly related to escalating trade concerns.

“As companies and countries race to secure supplies that may become expensive later on, exports have surged and inventories have swelled. If these trends are one-time adjustments (and our economists believe they are), the ‘payback’ in 2H could be significant. Enjoy the 2Q GDP number, which may be the last best print for a while.

The ‘stockpiling’ in exports could be responsible for 1.5 percentage points of our 4.7% 2Q GDP estimate. ‘Stockpiling’ also appears to be at work for US companies, albeit to a more limited extent. The inventory build in 2Q is tracking at +US$38 billion, versus a +US$10 billion rate in the prior two quarters. And what’s more interesting is the areas where those inventories are building, which have material overlaps with trade: electrical goods, machinery equipment, motor vehicles and parts.”

In other words, the contribution to Q2 GDP from inventories alone would be roughly 2.2%, or roughly 50%, of the total increase. Such would be the single biggest combined contribution since 4Q11 when the U.S. was restocking auto inventories following the tsunami-related shutdown of Japan.

These one-off adjustments are unsustainable and simply represent the pull-forward of demand that will be given back over the subsequent quarters. Following the economic reboot in Q4 of 2011, as Japan’s manufacturing came back online, the next five quarters averaged just 1.6%.'

The Mirage That Will Be Q2 GDP

In other words...the Q2 2018 GDP Growth will almost certainly be big when the initial numbers are released tomorrow.

BUT...as much as half of that GDP growth could be due to increases in inventories due to Trump's tariffs/the trade war fears.

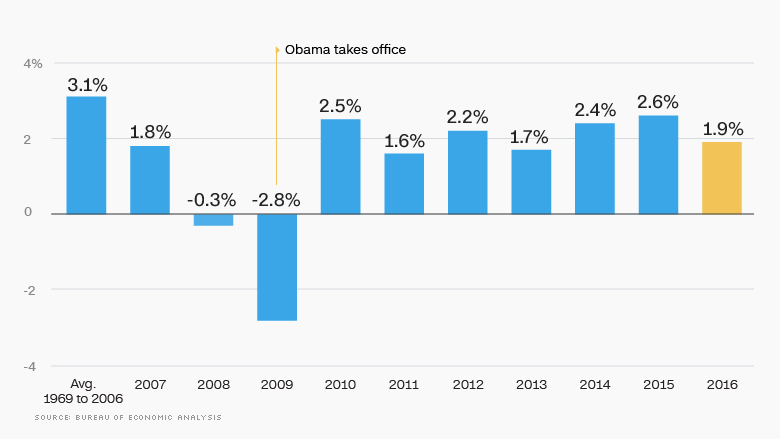

Conclusion? Tomorrow's numbers will probably be a one off. The economy will probably go back to growing at it's tepid pace by year end - since it has since Trump took over AND since 2009.

Once again...I am neither Dem nor Rep.

...

Secondly, while the print will undoubtedly be a strong one, and not unexpected following a weak Q1 growth rate, the question is whether it is sustainable? A recent note from Goldman Sachs suggests some caution:

“An unusually large number of one-off factors appear to have boosted 2Q GDP, many of which are directly related to escalating trade concerns. As companies and countries race to secure supplies that may become expensive later on, exports have surged and inventories have swelled. If these trends are one-time adjustments (and our economists believe they are), the ‘payback’ in 2H could be significant. Enjoy the 2Q GDP number, which may be the last best print for a while.”

This is likely correct. As 2018 has seen a steady increase in trade tensions, and trade actions, between the US and its trading partners, we have already begun to see some of the negative impacts from those actions. Just this past week Boeing ($BA), General Motors ($GM) and Whirlpool ($WHR) all had disappointing reports with comments directly related to the negative impact of tariffs on their results. They are surely not going to be the last as the US has slapped tariffs on washing machines and solar panels in January, on steel and aluminum in March, and on US$34 billion of goods from China on July 6. Now, the administration is talking about another 25% tariff on close to $200 billion in foreign-made automobiles later this year.

Morgan Stanley also made very similar comments in their recent analysis about the unusually large number of one-off factors which appear to have boosted 2Q GDP, most of which are directly related to escalating trade concerns.

“As companies and countries race to secure supplies that may become expensive later on, exports have surged and inventories have swelled. If these trends are one-time adjustments (and our economists believe they are), the ‘payback’ in 2H could be significant. Enjoy the 2Q GDP number, which may be the last best print for a while.

The ‘stockpiling’ in exports could be responsible for 1.5 percentage points of our 4.7% 2Q GDP estimate. ‘Stockpiling’ also appears to be at work for US companies, albeit to a more limited extent. The inventory build in 2Q is tracking at +US$38 billion, versus a +US$10 billion rate in the prior two quarters. And what’s more interesting is the areas where those inventories are building, which have material overlaps with trade: electrical goods, machinery equipment, motor vehicles and parts.”

In other words, the contribution to Q2 GDP from inventories alone would be roughly 2.2%, or roughly 50%, of the total increase. Such would be the single biggest combined contribution since 4Q11 when the U.S. was restocking auto inventories following the tsunami-related shutdown of Japan.

These one-off adjustments are unsustainable and simply represent the pull-forward of demand that will be given back over the subsequent quarters. Following the economic reboot in Q4 of 2011, as Japan’s manufacturing came back online, the next five quarters averaged just 1.6%.'

The Mirage That Will Be Q2 GDP

In other words...the Q2 2018 GDP Growth will almost certainly be big when the initial numbers are released tomorrow.

BUT...as much as half of that GDP growth could be due to increases in inventories due to Trump's tariffs/the trade war fears.

Conclusion? Tomorrow's numbers will probably be a one off. The economy will probably go back to growing at it's tepid pace by year end - since it has since Trump took over AND since 2009.

Once again...I am neither Dem nor Rep.

Last edited: